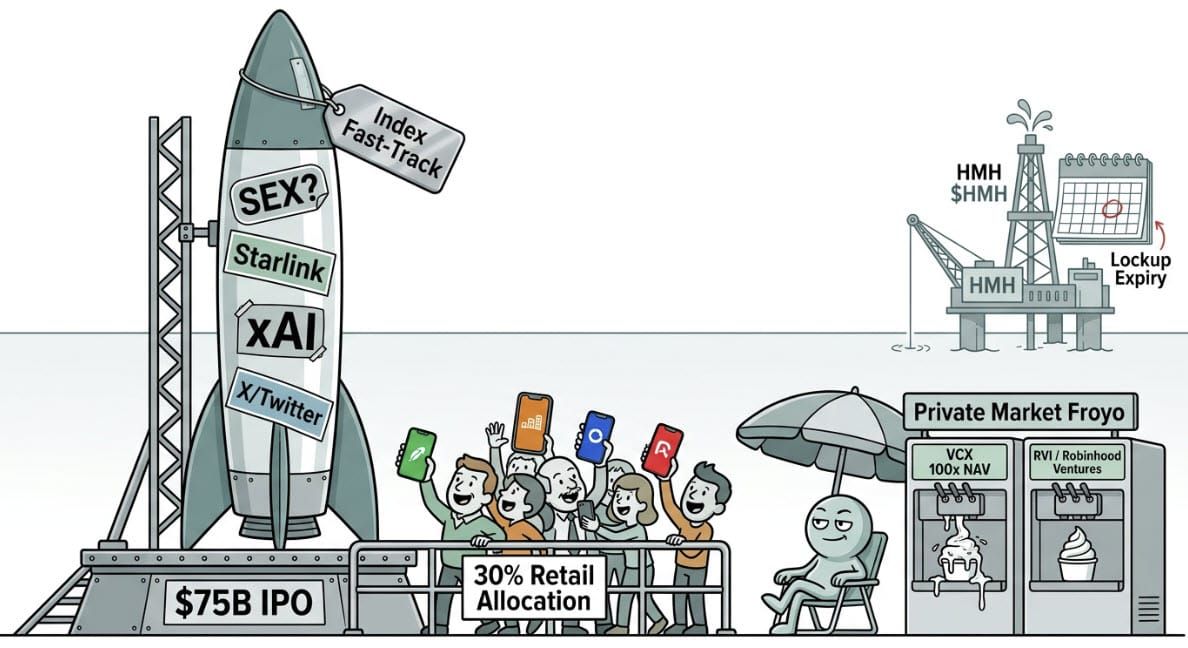

The SpaceX $SPCX IPO is upon us. The S-1 was filed and there is rampant commentary on it already. We don't have pricing and valuation information yet but the loose $1.5T number relies in large part on the "optionality" from not-yet-existent businesses.

There are quite a few salient risk factors (including the 90-day out Anthropic has on the $1.25B/month they are paying for capacity.) Even the core Starlink business has some concerning trends, especially a steady decline in ARPU as they grow.

If there is a "single point of failure" it's Starship execution (the next launch is scheduled for tonight after it scrubbed yesterday.) I've never seen such an important event so closely aligned with a public market debut but here we are.

Here's a link to the launch to stay informed. The bankers will be watching!

The success of Starship is needed to boost the Starlink business AND validate the optionality argument around future revenues from orbital AI, a potential "terafab," and more advanced missions to the Moon and Mars.

Starship would reduce launch costs and can deploy 60 new V3 satellites with up to a 1TB/s downlink each. That's a 20x improvement in capacity per launch versus Falcon 9. That feeds into allowing Starlink to continue to grow rapidly with lower ARPU yet still have attractive margins.

Space Feeds AI

If we do get a Starship success it will lead to more robust connectivity and space businesses that will be used to fund continued investment into the xAI/Grok/X segment.

The AI segment strategy remains unclear in terms of margins (currently negative ~200%) and ongoing capital expenses. It's possible that the "story" of this business will be more along the lines of a support mission that adds to the moat the company has in the profitable businesses and not thought about as a standalone LOB.

Outside of Starship the top tier real risks are the contracted revenue from Anthropic, regulatory exposure/risk and of course the "governance" factor which can cut both ways with retail investors preferring an "everything Elon" structure. Of course that does put a lot of market cap on the ongoing performance of an individual.

Estimates vary but a rough rule of thumb is that about half of the valuation will be based on Starlink/Space and the other half we be about whatever percentage of the science fiction appears viable.

The roadshow and slides should drop soon!

{kind=link}