PACS Group $PACS priced an upsized deal of 19M shares at the mid-point of $21. Using 148M shares, the market value is $3.1B or 1x revenue.

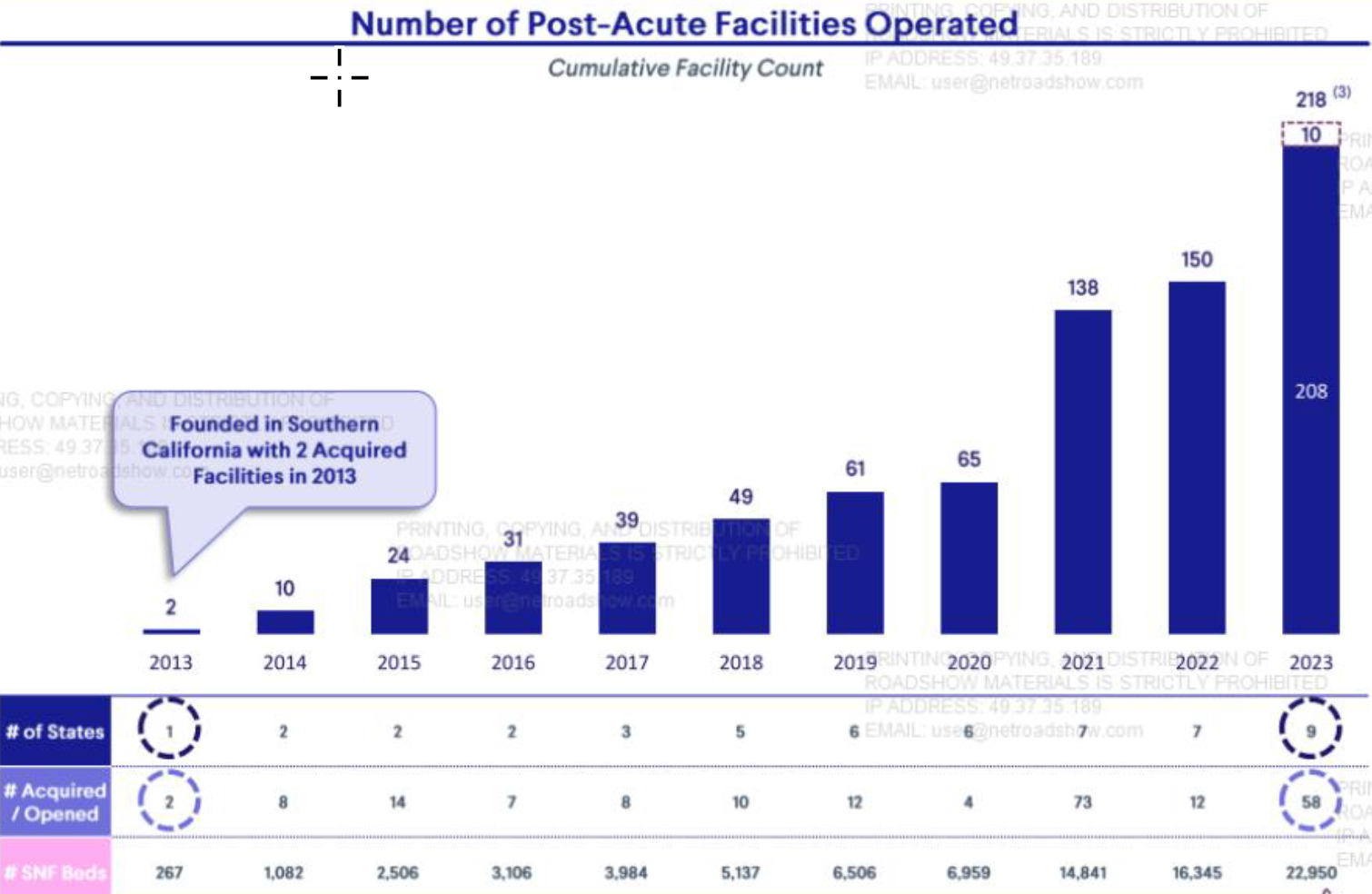

PACS has been rolling up and post-acute care facilities since 2013. After starting with 2 in Southern California, they have reached a critical mass and proven their operating model and abilities.

PACS invests in acquired facilities to upgrade staff, operating methods, fixed assets, technology, and systems. This is reflected in ratings that move up to 4 stars or higher.

Improving facilities in terms of conditions and clinical effectiveness results in higher utilization and greater profitability. (Much as a hotel would by going from 70% occupancy to 90%.)

Most of PACS revenue comes from Medicaid and Medicare (76%) and is also impacted by other government agency actions. Organizations like CMS and HHS can be inscrutable. They may contribute to some volatility of PACS revenues and margins, but these should be nominal.

Debt will be reduced with the IPO proceeds but will be an ongoing and important part of operations. Interest expenses have grown substantially and were $50M in 2023 compared to net income of $113M.

Litigation and claims settlement expenses have also been a drag on operating margins. This is partly due to one major acquisition (Plum) that was done as a business combination. This accounted for $27M of the $39M total spent on this area in 2023.

Executive compensation has been unusually high. The co-founders were paying themselves $3M/year in salary. Then, they added $4M a year of payments to a consulting firm they founded (Helios) to provide "consulting and strategic advisory services."

With the IPO, they revert to more conventional compensation levels but continue to own 87% of the company shares, so they will be well compensated.

Stock Conclusion

PACS is unlikely to make our list of followed companies. The company is very closely held by the founders, who have been busy lining their pockets along the way.

A heavy regulatory backdrop and complex and ongoing debt arrangements are not areas in which we're looking to spend more time.

There is plenty of market opportunity in terms of growth. The existing industry is huge and fragmented, and demographics will drive a greater need for post-acute care facilities.

However, there are some notable headwinds for PACS - 1) interest rates are a significant cost, and it's unclear they are heading lower, and 2) wage inflation, particularly in the healthcare industry, is robust.

The initial valuation of 1x sales is fairly in line with comparable companies. The same is true for EV/EBITDA using a "normalized" 10% margin based on their long-term guidance.

We may look again after they print a few quarters and we get a look at what their post-IPO growth is versus their guidance of ~ mid-teens revenue growth.

In this general category, we're taking another look at GoHealth $GOCO, which has been making some strong progress in Medicare insurance that investors have yet to give them credit for. At 1x current sales, I think they have more upside.

{kind=link}