Rubrik $RBRK will be priced tomorrow and begin trading on Thursday. It's a hefty ~$700M offering (23M shares @ $28 - $31). At the midpoint, the market cap will be $5.3B.

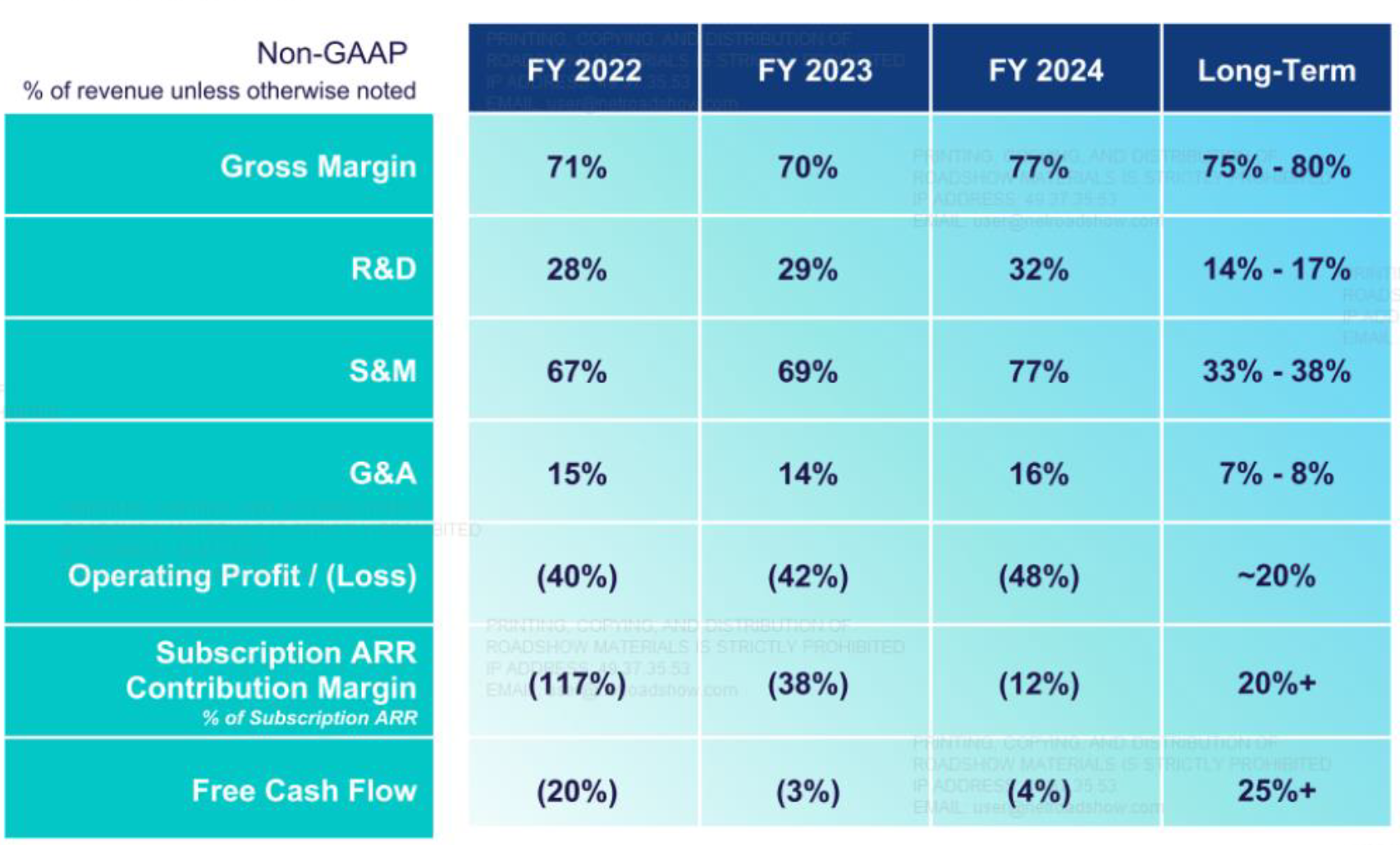

Revenues for the year ended January 2024 were $628M, with an operating loss of $306M. Since this is an enterprise SaaS business, investors should not pay attention to the current P&L.

Data Backup and Restore is now "Cyber Recovery."

This has been a good business for a long time. Data is critical to every enterprise, and management tools are critical to any IT infrastructure. Veritas was the first large public player in this market decades ago. As further proof of the value of this business, consider that Veritas just changed hands again this year at $7B!

Rubrik is taking it one step further and striving to be more of a "data security" company. They wish to position themselves closer to a Palo Alto $PANW, Crowdstrike $CRWD, and ZScaler $ZS than a Commvault $CVLT.

Rubrik has a suite of tools that help protect and manage data and, more importantly, restore and recover rapidly from data loss. Ransomware has penetrated the psyche of most large organizations, and they are willing to write checks to protect themselves further.

There are some minor bits of interesting technology here regarding using meta-data more effectively, but it's not an exciting segment of enterprise IT for me. Later this year or in 2025 we will probably see Veritas back in the public markets as a part of Cohesity's IPO.

Valuation

Bankers will note that 8.4x sales are "cheap" relative to other leading enterprise SaaS companies trading at 11x to 17x sales.

These companies are profitable though while Rubrik will be losing money for some time to come, especially if one includes SBC.

We can also consider "normalized earnings" informed by the long-term model offered below.

Leading enterprise security SaaS P/E multiples are 52x to 76x. If we apply a 20% operating margin to $700M of revenue, we get $140M in earnings.

Using the multiples above, we can sketch out a valuation of $7B to $12B at the upper end. Regarding a stock price, that's ~ $40 to $60/share.

Rubrik still has a lot of wood to chop vis a vis the current P&L and the long-term model. Other enterprise SaaS names have tended to tread water until they reach profitability. Rubrik is fairly large, though, and is closing in on $1B in revenue. If they can make rapid progress toward better margins, we'd be more interested.

{kind=link}