Last week we had another "AI Biotech" name Generate Biomedicines $GENB stumble into public markets with a middle-of-the-range price of $16 and break to $13 immediately after. In the past several years it's become clearer to investors that the path to a new drug doesn't matter much relative to the value of the approved drug itself which tends to accrue to the large pharma companies.

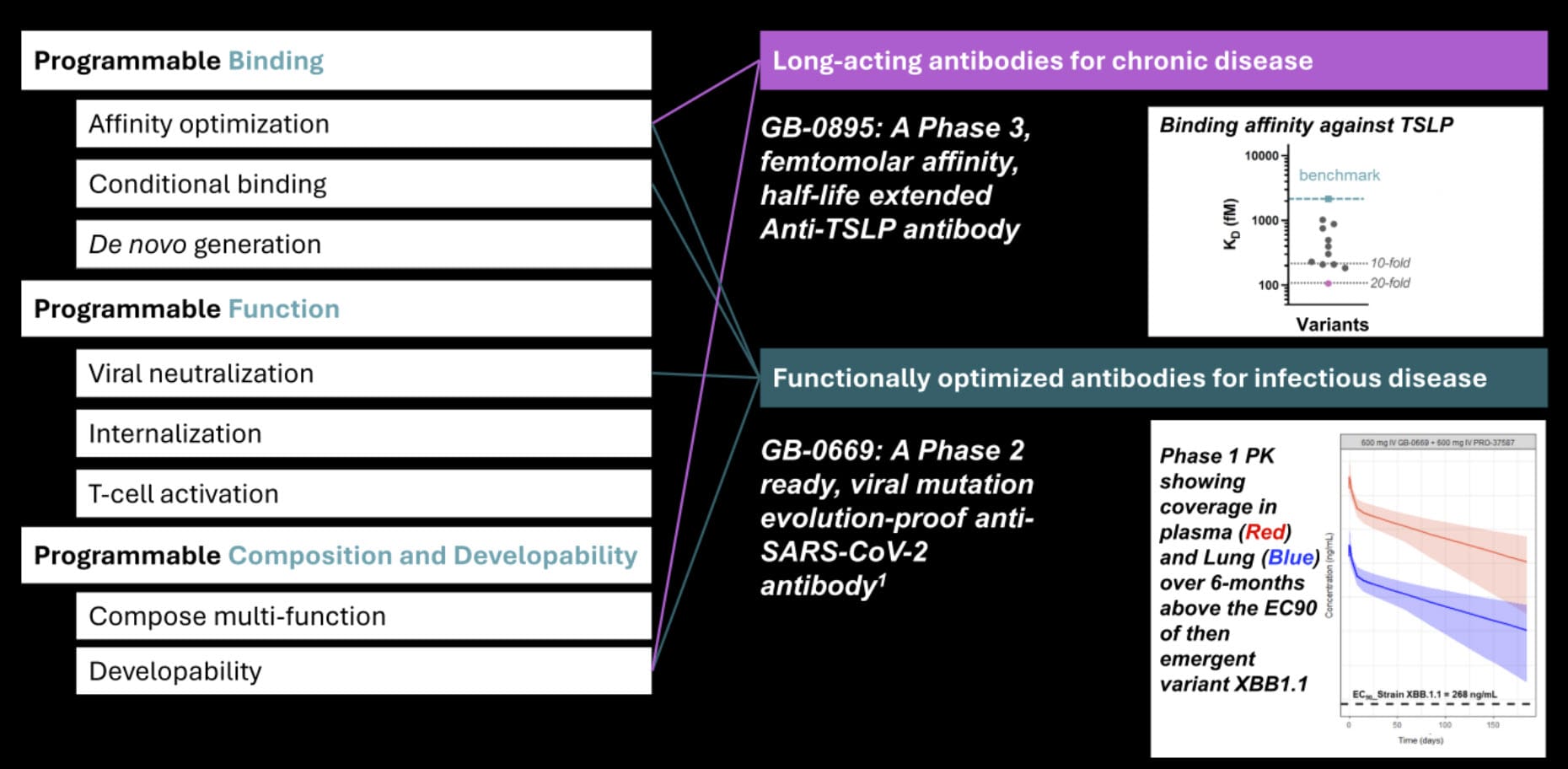

Although the IPO itself wasn't compelling there were two AI-based wrinkles that are worth noting. The first was a division and separation of molecular function, binding and composition/development. The second was the clear intention and benefit of having proprietary structural data that can only be used to inform in-house models.

Why is that important? The AI frenzy should serve as a reminder that proprietary data/information will be a critical long-term advantage. By this I mean not content that can be licensed or sourced elsewhere. It means you need to identify and protect what you have including building whatever infrastructure is need to keep it from being discovered. GENB illustrates their ability to get better results with their in-house structures.

The explicit division and separation of the process also seems promising. It can probably be implemented by other AI biotech platforms like Schrodinger $SDGR but it help to accelerate useful drug development.

GENB has one drug entering Phase 3 (for Asthma) and a few others in early development. They have strong partnerships and financing from major pharma companies so it could work out. The Phase 3 readout on GB-0895 will be the big catalyst which can send the stock to $8 or $30. Envelope please!

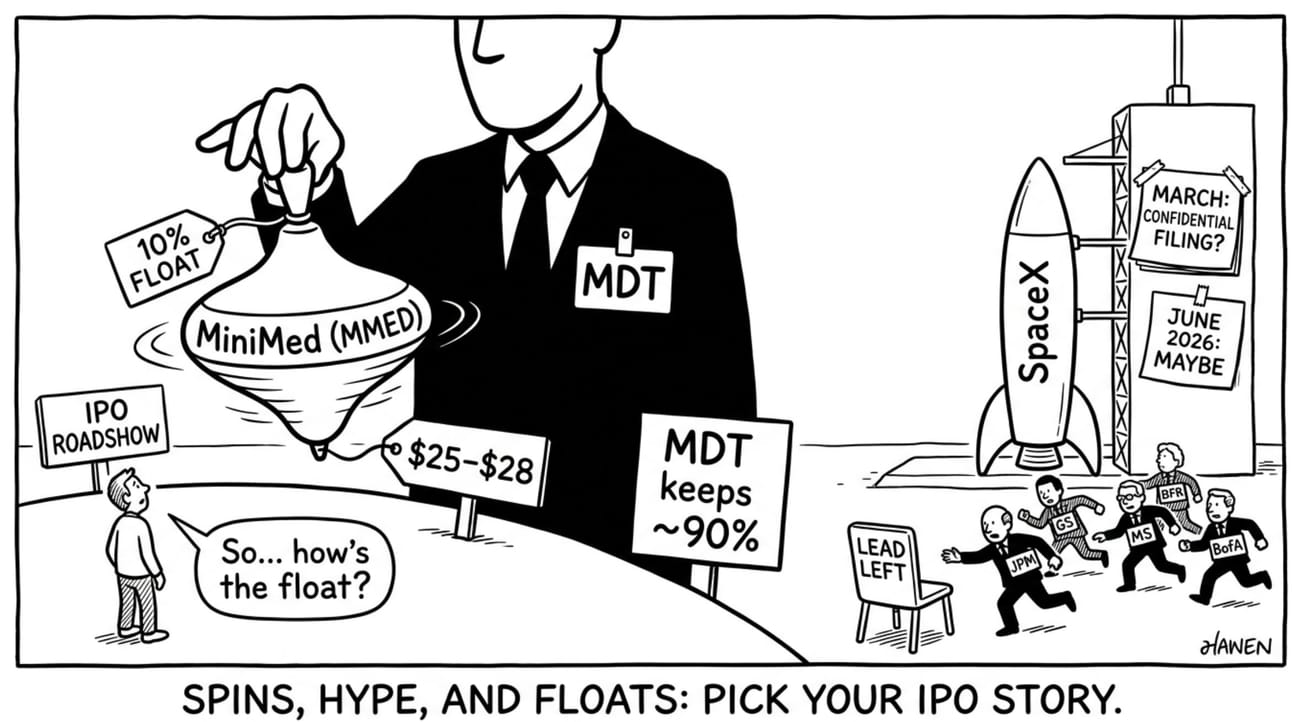

Medtronic Spins MiniMed

Medtronic $MDT bought MiniMed in 2001 for $3.7B. If it prices in the range the EV will be just over $7B. They are only selling 10% so investors will have to ponder to what degree this represents an overhang post-IPO.

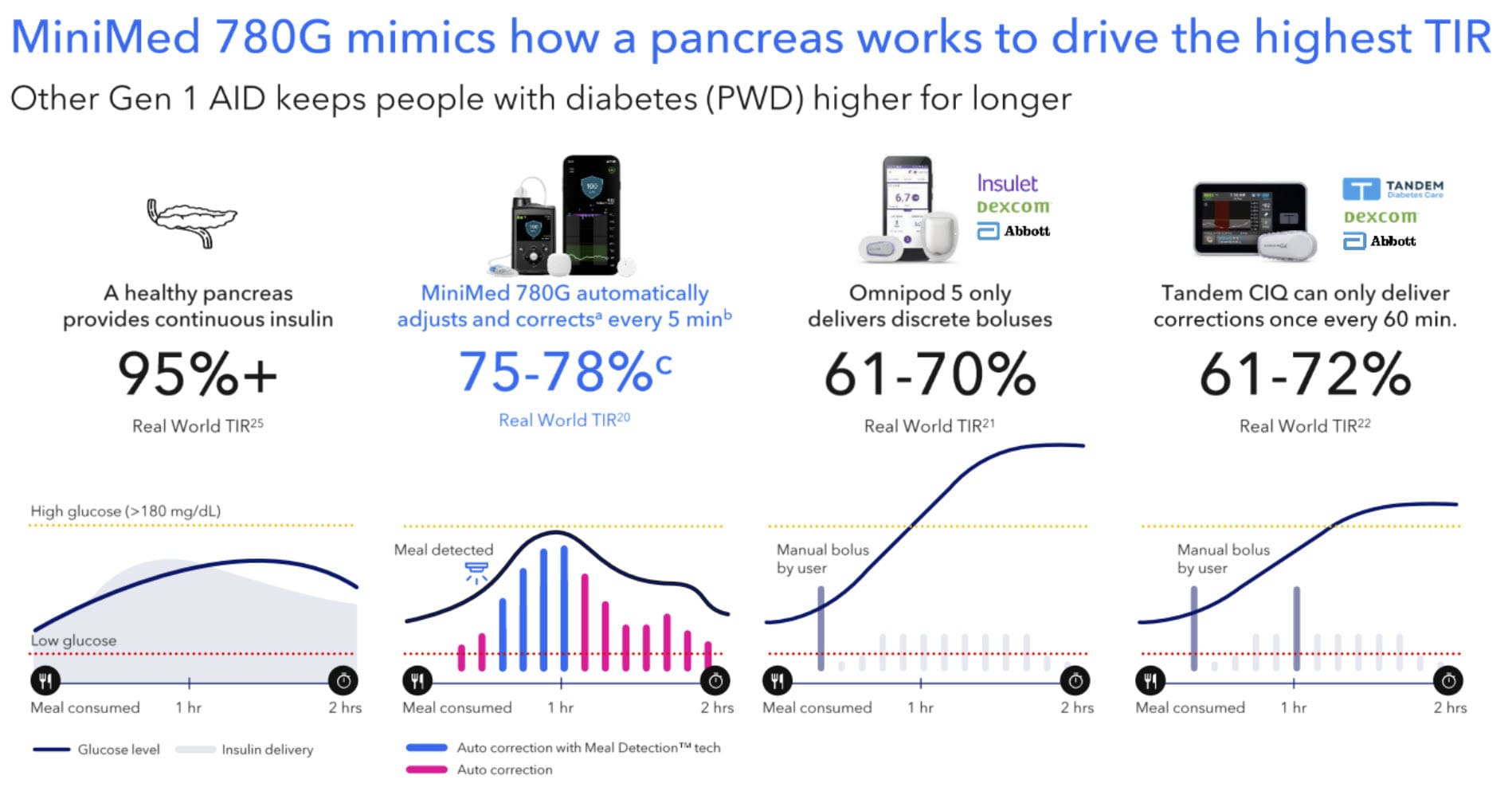

MiniMed $MMED did $2.7B in revenue last year with $1.5B in GP and positive EBITDA. This is all about diabetes and the quest to provide a solution as close to a healthy pancreas as possible to increase healthy levels of glucose. A key measure is Time in Range (TIR).

The challenge for diabetics is to administer insulin just right and it involves delays and guesswork in terms of timing and dosage. Constant glucose monitors (CGMs) help and so do discrete dosage units and periodic delivery. Companies like Abbott $ABT, Dexcom $DXCM, Insulet $PODD and Tandem Diabetes $TNDM are well known in the space.

MiniMed promises a better solution with improved TIR. It's not quite a healthy pancreas but it's something. It might be worth a deeper dive but at this point the broad strokes might be enough - at $7B it's under 3x sales with peers in the 4-5x range so it's not a demanding price and should work.

Fundamentals may be subordinate to the MDT plan for the rest of the shares. The preferred path is an exchange offer for existing MDT shareholders but the timing, mechanics and pricing will be important.

SpaceX IPO

With all they hype surrounding the SpaceX IPO it's worth keeping a firm handle on what is or isn't happening. Popular press is teasing a "March IPO" for the company which is unrealistic.

As a reminder the timeline is oriented toward a June 2026 potential IPO date which means a confidential filing could happen in March but that's all.

The company is also facing some challenges because the deal size and valuation will want institutional participation (even though retail demand is likely to be rabid) and governance issues are a bit thorny.

Investors will also be parsing a unique business with a steady recurring business (Starlink) funding an aspirational, often immolating business of rockets.

The usual suspects (Goldman, BofA, JPM and Morgan Stanley) are all competing for the "lead left" position on the deal. Don't expect any restraint from the underwriters in terms of the IPO hype cycle.

{kind=link}